KATHMANDU — Sometime on April 28, 2026, the state treasury of Nepal pulled off a masterclass in financial smoke and mirrors.

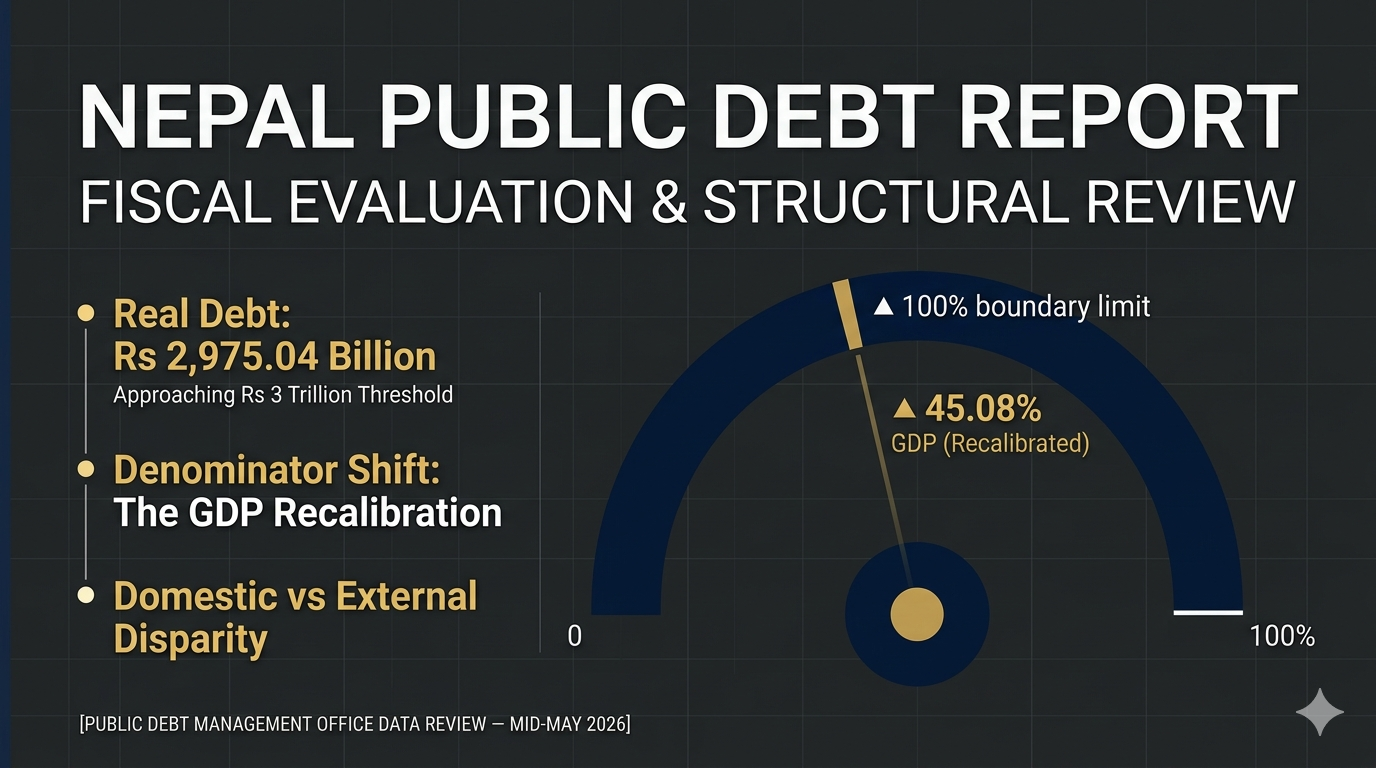

If you glance at the latest mid-May data released by the Public Debt Management Office (PDMO), Nepal’s public debt-to-GDP ratio appears to have miraculously dropped from a dangerous 48.04% in April down to a highly respectable 45.08%.

But don’t let the charts deceive you: the government didn’t settle its tabs or pay off its lenders. Instead, the National Statistics Office simply adjusted the nation’s annual GDP estimates upward. By artificially inflating the baseline size of the economy (the mathematical denominator), the government made its soaring liabilities look smaller on paper.

The harsh, cash-in-hand truth? Nepal’s real public debt has surged to an unprecedented Rs 2,975.04 billion—putting the nation just inches away from crossing the staggering Rs 3 trillion threshold. Over the last ten months, the government has been packing on an average of Rs 30 billion in fresh debt every single month just to stay solvent.

Cannibalizing Local Credit: The Domestic Squeeze

Perhaps the most telling sign of Nepal’s internal fragility is where this new money is being sourced.

The state originally planned to raise a total of Rs 595.66 billion in loans for the fiscal year. So far, they have secured 61.30% of that goal (Rs 365.16 billion). However, the composition of this capital reveals a deeply troubling trend:

Domestic Borrowing: The state has already aggressively drained 82.50% (Rs 298.67 billion) of its entire annual internal target.

External Borrowing: In sharp contrast, international funds from foreign lenders have slowed to a crawl, hitting a mere 28.46% (Rs 66.49 billion) of the target.

Because complex bureaucratic delays prevent the state from hitting the construction milestones required to unlock foreign aid, the government has turned inward. Local commercial banks are being systematically drained of liquidity through Treasury bills and development bonds to fund day-to-day bureaucratic operations. This relentless domestic push directly “crowds out” the private sector, starving small businesses and local industries of the credit they need to scale up and generate employment.

The Exchange Rate Penalty: Paying Billions for Thin Air

Nepal’s growing debt crisis isn’t just a byproduct of over-borrowing—it is also being heavily driven by global currency volatility.

The Exchange Loss Fact: Over the course of the fiscal year, the Nepali Rupee plummeted from roughly Rs 137 per US dollar in mid-July 2025 to historic lows of nearly Rs 150 per dollar by May.

Because over 70% of Nepal’s external debt is denominated in Special Drawing Rights (SDR) and another 20% is held in US Dollars, the rapid devaluation of the rupee has wreaked havoc on the balance sheet. Without receiving a single new dollar to pave a highway or construct a power line, currency depreciation alone automatically tacked an unprompted Rs 115.75 billion in pure exchange rate losses onto our international liabilities earlier this quarter.

The Servicing Cycle: A Treasury Chasing its Own Tail

To understand how close the country is to a genuine debt trap, one only needs to look at where the cash goes once it’s raised.

Over the last ten months, the government has funneled Rs 258.44 billion straight back out of the treasury to handle debt servicing—repaying principal and interest on older loans. This massive cash drainage consumes 4.23% of Nepal’s entire GDP.

The state is effectively trapped in a vicious cycle: it is issuing massive amounts of high-interest internal bonds today simply to pay back the maturing debts of yesterday. Meanwhile, capital expenditure—the actual money spent on infrastructure that drives real, long-term economic growth—remains chronically neglected, with less than a quarter of the development budget actually deployed by the spring.

With state oversight bodies like the National Natural Resources and Fiscal Commission (NNRFC) loudly calling for an absolute ban on using domestic loans to cover recurrent government costs, the upcoming federal budget will be a definitive test. If the state continues to use long-term debt as a revolving credit card to fund its administrative machinery, the Rs 3 trillion milestone won’t just be an alarming statistic—it will be the moment the trap door firmly locks.